Compliance to the code Ahold Delhaize

PDF, 122 kB

At Ahold Delhaize, we seek to make a positive impact in the communities where our brands operate and be good neighbors. We do this by paying taxes in a way that takes into consideration social and corporate responsibility and the interests of all our stakeholders. Our overall tax approach is in line with Ahold Delhaize’s Business Principles, ESG strategy and Code of Conduct.

Our tax policy, which applies to all consolidated group entities, consists of five main tax principles: transparency, accountability and governance, compliance, relationships with authorities and business structure. Our tax principles are aligned with The B Team’s Responsible Tax Principles, developed by a group of leading companies, with involvement from civil society, investors and representatives from international institutions. In 2017, The B Team brought together the heads of Tax from nine multinationals to develop the Responsible Tax Principles, which raise the bar on how businesses approach tax and transparency and help forge a new consensus around what responsible tax practice looks like.

Ahold Delhaize complies with the principles included in the VNO-NCW Tax Governance Code.

For further reference to how Ahold Delhaize complies with the Tax Governance Code, please refer to the document below.

By paying our share of taxes in the countries where we have operations, we contribute to economic and social development in these countries. Also, with our total tax contribution, we support the UN SDGs.

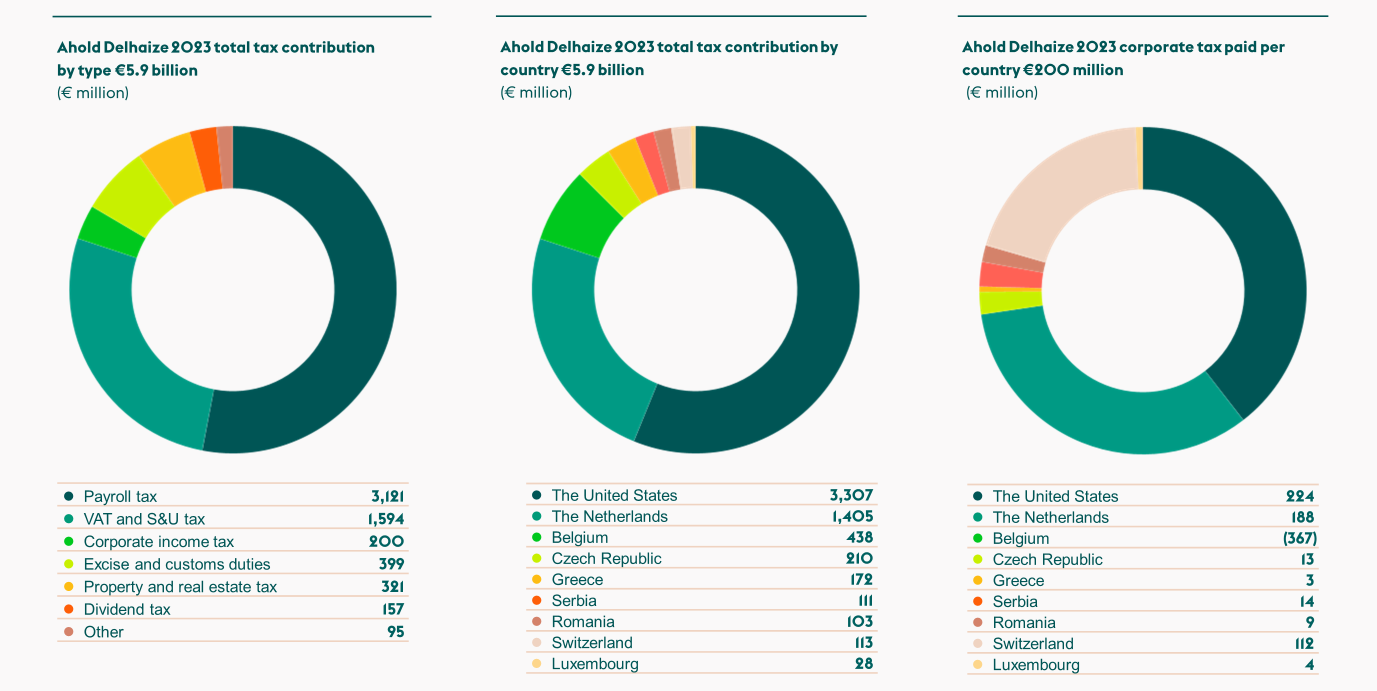

In 2023, Ahold Delhaize collected and bore many types of taxes: payroll tax, corporate income tax, net-value-added tax (VAT), sales and use (S&U) tax, property tax and real estate tax, dividend tax, excise and customs duties and others (e.g., packaging tax), for a total amount of €5.9 billion. Approximately €1.7 billion of the company’s total tax contribution in 2023 was taxes borne.

The total tax contribution and corporate income tax payments that were reported per country are summarized below.

Our effective income tax rate (ETR) over 2023 was 19.8%. This is our worldwide income tax expense for the financial year 2023, amounting to €456 million, shown as a percentage of the consolidated income before income taxes.

We define tax incentives as fiscal measures designed by governments to stimulate investment and encourage growth or a change in behavior by providing more favorable tax treatment to some activities or sectors.

For some of the activities that Ahold Delhaize and the brands undertake as part of our efforts to positively impact communities, there are tax incentives available, as described below.

Ahold Delhaize does make limited use of tax incentives. The main tax incentives applied by Ahold Delhaize in the various jurisdictions where our brands operate are:

Wage tax credits

Certain wage tax credits are available to companies that give opportunities to people who normally face difficulties finding employment, such as individuals with physical disabilities, as local governments seek to stimulate work participation in the labor market for these employees.

Capital investment credits

Local governments sometimes provide capital investment credits to stimulate investment (e.g., in warehouses or stores) in certain areas, to stimulate economic growth in their local communities.

Research & Development (R&D) incentives

Local governments sometimes provide R&D incentives to companies undertaking certain activities that increase the level of innovation and economic growth in their communities. We are always striving to innovate as we drive operational excellence, for instance, by optimizing stock in our brands’ DCs and stores. We receive R&D incentives for some of these activities.

Ahold Delhaize has a well-equipped and professional Tax function. It reports directly to the CFO and has direct access to the Management Board and the Supervisory Board. At least once a year, the function presents a tax update, including the implementation and execution of the tax strategy, to the Audit, Finance and Risk Committee of the Supervisory Board. The global tax policy is approved by the Management Board.

Our tax risk appetite is based on Ahold Delhaize’s overall compliance-related risk appetite, which is very low. We recognize the risk that non-compliance with applicable tax laws and regulations could result in damage to Ahold Delhaize’s reputation or to the relationship with our host countries.

Being in control in relation to taxes and responsible taxation is an important objective for our Tax department and our Company. We have certain activities in place to support this, including:

Each quarter, our brands sign a letter of representation, which includes an approval and a confirmation on the accuracy and completeness of our tax position. We have a tax strategy in place that is proactively communicated throughout the Company, and we organize training for selected brands and jurisdictions, during which the tax policy and its main principles are explained through tax risk workshops.

On a regular basis, we monitor whether our tax strategy is aligned with the Ahold Delhaize Business Principles, ESG strategy and Code of Conduct. For example, the Tax department’s annual objectives are based on the abovementioned principles and strategy and cascaded to individual associates’ goals. Department and associate performance compared to these objectives is measured at least once per year.

Ahold Delhaize associates have access to a whistle-blower line for reporting any ethical or compliance concerns related to company practices, including tax matters.

We are also actively involved in the field of tax technology. We have drafted a global tax technology strategy and roadmap based on five pillars: insights, data driven, automation, risk management and future proof. We set up various initiatives within our direct tax disciplines (such as country-by-country reporting automation, Pillar 2 calculations and a tax reporting engine) and indirect tax disciplines (such as a VAT solution and tax engine), to optimize and upgrade our tax processes. We closely align with broader finance implementations, such as a new core finance system, and our IT function assists us with our tax technology projects.

Our tax compliance is based on the following examples of good tax practices:

Ahold Delhaize engages with tax authorities based on mutual trust, and we seek open and transparent working relationships with them. We provide the tax authorities with any information they require within a reasonable timeframe. This helps both the tax authorities and Ahold Delhaize to foster timely and efficient compliance. In the Netherlands, we have an individual monitoring plan in place with the Dutch tax authorities. In Belgium, we successfully finalized the Co-operative Tax Compliance Program (CTCP) pilot project in 2023.

As a company close to society, we value constructive dialogue on taxes with the governments in the countries where our brands operate and we respond to government consultations on proposed changes to legislation with the aim to achieve sustainable legislation.

In addition to the tax authorities, our stakeholders also include investors, customers, business partners, non-governmental organizations, employees and the broader communities in which we operate. We are an active member in a number of stakeholder representation groups such as the VNO-NCW and Nederlandse Orde van Belastingadviseurs. We also participate and provide active feedback in the Dutch Association of Investors for Sustainable Development (VBDO) tax transparency initiative. We actively participate in the European Business Tax Forum (EBTF) Total Tax Contribution Study.

We have a physical presence in all jurisdictions where we operate and we follow internationally accepted norms and standards (e.g., OECD)/Action Plan on Base Erosion and Profit Shifting/EU).

In anticipation of new EU and OECD regulations (e.g., Pillar 2), we ceased operations in Curacao at the end of 2023 and transferred the remaining activities in Curacao to other Ahold Delhaize operations at the first day of the new financial year 2024. We do not expect material changes for any of our other operations with respect to Pillar 2 implementation.

Our tax decision-making process is based on the following examples of good tax practices: